In addition to their liquidity management and cybersecurity benefits, new payment models such as virtual accounts and digital wallets can improve accounts payable (A/P) and accounts receivable (A/R) processes.

These improvements center on facilitating and streamlining the connectivity among A/P, A/R, and liquidity management activities. However, the magnitude of these improvements and other benefits depends on how well corporate treasury teams, their IT colleagues, and external banking partners address complexity and other challenges posed by new advances in payments.

"For corporate treasury groups, digital wallets to handle cybercurrency were discussed by a small percentage of companies just a few years back," recalls Strategic Treasurer managing partner Craig Jeffery. "Today, the discussions are real and centered on particular use cases that frequently reflect additional [revenue-related] business opportunities, and more treasury groups are exploring them in earnest instead of merely talking about them as a concept."

Deloitte Consulting transaction banking practice leader Michelle Gauchat notes that virtual accounts offer "significantly faster turnaround time for corporate entities," especially for larger companies that typically maintain large numbers of bank accounts. "Opening a virtual account with the right platform can happen in a couple of minutes, and virtual accounts can be closed easily," Gauchat continues. "Virtual accounts help in consolidating funds in real time and offer better reporting and reconciliation."

Ernst & Young LLP partner/principal Kasif Wadiwala notes that virtual accounts also help corporate treasury functions strengthen liquidity management and fraud prevention while reducing banking fees and related costs. He says that digital wallets can help treasury teams comply with the Payment Card Industry Data Security Standard (PCI DSS) and other requirements, while also equipping them with "access to greater strategic insights that can be used to further refine their credit control processes."

Additionally, many new accelerated-payment platforms use the ISO 20022 messaging format, which allows for more data to be transmitted quicker. These speed and volume increases help corporate treasury functions enhance reconciliations and cash forecast variance assessments, notes Deloitte Risk & Financial Advisory principal Prashant Patri.

To maximize those benefits, corporate treasury functions should recognize and address challenges associated with virtual accounts and digital wallets. Most of these hurdles relate to technology integration and upgrades, although fraud and compliance challenges also arise, as well as a lack of awareness among trading partners.

New applications require appropriate fraud controls at a point when cybersecurity marks a growing concern among corporate treasurers: Forty-five percent of 245 treasury executives who responded to Deloitte's "2022 Global Corporate Treasury Survey" ranked security and controls as part of one of their top five challenges. "During the pandemic, companies have been more exposed to payment fraud," according to Deloitte's survey report. "While treasury systems and banking platforms tend to comply with security requirements of most organizations, fraud usually occurs through phishing emails, ad hoc payment requests, social engineering, or even internal fraud."

Another challenge is that, despite these payment methods' growing use, many customers and even suppliers remain unaware of them. Treasury teams may find that the suppliers they would like to pay using these techniques, or the customers they are offering new payment options, may need to be educated on the value that these payment modes offer, notes Wadiwala. Digital wallet usage must satisfy a range of financial industry compliance requirements as well as consumer-focused regulations. Virtual accounts are also subject to a "shifting set of regulatory and compliance restrictions that impact their usage—for both banks and corporates—in certain localities," Wadiwala notes.

Treasury functions and their banking partners face technology-related challenges associated with virtual accounts and accelerated payments more broadly. On the corporate side, integration issues often loom large. Many organizations need to update their technology infrastructure to support real-time payments, notes Gauchat. This often includes the use of application programming interfaces (APIs) to support host-to-host (H2H) connectivity—which enables high volumes of data to be transferred in an automated manner (vs. a file upload) between companies and their banking partners.

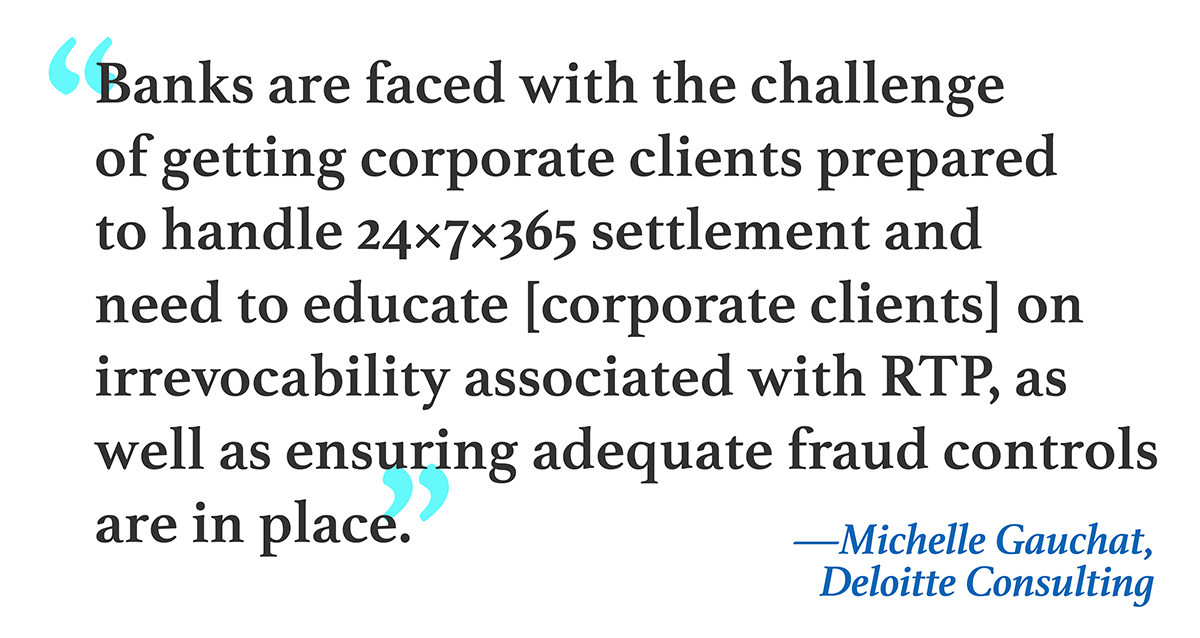

Banks also have work to do. "Banks supporting new payment types must upgrade their infrastructure to support real-time processing, especially when volumes increase multifold," Gauchat notes. "Most of the existing infrastructure does not support extensive real-time processing. Banks are also faced with the challenge of getting corporate clients prepared to handle 24×7×365 settlement and need to work with clients to educate them on irrevocability associated with RTP [Real-Time Payments], as well as ensuring adequate fraud controls are in place."

Some banks also need to update their infrastructure platforms to support the ISO 20022 format and to prevent the need to translate among multiple messaging standards while processing payment transactions.

See also:

- November 2022 Special Report

- Accelerated Payments: Key Considerations

- Next-Level Efficiency Opportunities for A/R and A/P

- Payment Innovations on the Horizon

Eric Krell's work has appeared previously in Treasury & Risk, as well as Consulting Magazine. He is based in Austin, Texas.

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.