As anyone who regularly deals with supply chain issues knows, buyers and suppliers of goods and services usually have conflicting interests. Supply chain managers at most companies are under pressure to improve the company's cash efficiency, usually by extending payment terms to their suppliers. But many suppliers lack the financial strength or flexibility to adjust to longer payment terms. For example, if a supplier already has a highly leveraged balance sheet, increasing bank borrowing to finance short-term working capital may be prohibitively expensive. Extended payment terms may also expose suppliers to increased commodity or foreign exchange risk.

As anyone who regularly deals with supply chain issues knows, buyers and suppliers of goods and services usually have conflicting interests. Supply chain managers at most companies are under pressure to improve the company's cash efficiency, usually by extending payment terms to their suppliers. But many suppliers lack the financial strength or flexibility to adjust to longer payment terms. For example, if a supplier already has a highly leveraged balance sheet, increasing bank borrowing to finance short-term working capital may be prohibitively expensive. Extended payment terms may also expose suppliers to increased commodity or foreign exchange risk.

When a large, well-capitalized company is buying goods or services from a small or highly leveraged supplier, it may be in a position to use its own balance sheet to support the supplier. A number of strategies have emerged in recent years to help buyers and suppliers leverage the buyer's stronger financial position to help the supplier access lower-cost liquidity, often so that the supplier can then offer the buyer extended payment terms. Most of these strategies involve monetization of the supplier's trade accounts receivable.

The most common forms of trade receivables monetization include open-account–based supply chain finance and negotiable-instrument–based supply chain finance. Together, these two strategies are often referred to as “structured vendor-payables finance” or “reverse factoring.” A third, related strategy is non-recourse receivables purchase, which is often incorrectly referred to as “factoring.”

How Open-Account Supply Chain Finance Works

An open-account structured vendor-payables program involves the sale of receivables owned by various suppliers and owed by one particular buyer. The suppliers sign up to negotiate and sell their receivables to investors via a bank or another company running an Internet-based platform. To maximize economies of scale, a buyer usually wants to have a number of suppliers taking part in its open-account program.

Depending on the size of the supplier base, the investors purchasing the receivables generally consist of a single bank or a small group of banks, although receivables are sometimes sold on a blind trading platform, in which case they may be purchased by any number of investors. The universe of possible investors is usually made up of the relationship banks of the buyer, but this is not always the case. In recent years, a number of alternative investors such as hedge funds and insurance companies have also appeared in the market.

Depending on the size of the supplier base, the investors purchasing the receivables generally consist of a single bank or a small group of banks, although receivables are sometimes sold on a blind trading platform, in which case they may be purchased by any number of investors. The universe of possible investors is usually made up of the relationship banks of the buyer, but this is not always the case. In recent years, a number of alternative investors such as hedge funds and insurance companies have also appeared in the market.

The platforms on which receivables are submitted, approved, and sold tend to be similar across most open-account structured vendor-payables programs. A supplier will sell goods or services to the buyer, generating an invoice that it posts on the supply chain finance platform for the buyer's confirmation. Once the buyer confirms the invoice as valid, the related receivable becomes eligible for purchase by an investor. Only confirmed invoices are eligible for purchase, so a specific transaction can be sold only if both the supplier and the buyer agree to have it sold.

In confirming the invoice, the original transaction's buyer agrees that it will pay the investor the full amount of the invoice on its due date without any claim, abatement, deduction, reduction, or offset of any kind. This confirmation enables the investor to look directly to the buyer for payment. The buyer may still request deductions and make similar claims against the supplier, with those offsets potentially applying to future invoices, but the buyer will not be permitted to challenge the amount owed on the receivable sold to the investor.

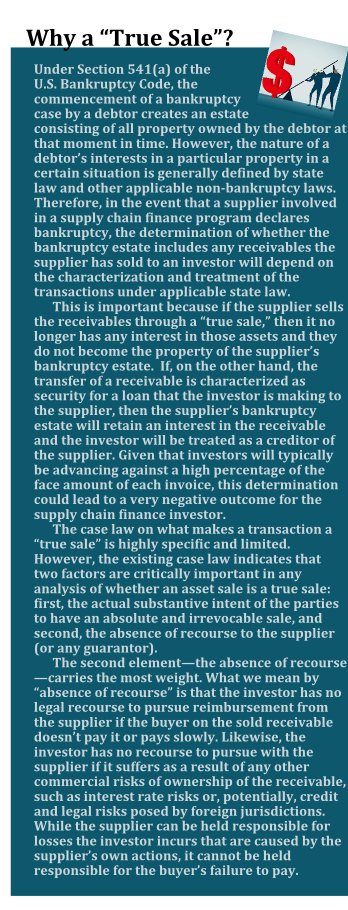

The investor's agreement with the supplier sets out a formula for determining the purchase price on all offered invoices. Typically the price is equal to the face value of the invoice minus a discount calculated based on the credit profile of the buyer—not the supplier—as well as the number of days to maturity of the receivable. If the supplier and investor elect to consummate the sale of a particular invoice, then the receivable represented by the invoice is sold on a non-recourse basis to the investor in a legal “true sale.” (See the sidebar Why a “True Sale”?) By utilizing a true sale, the investor can generally focus its underwriting on the underlying credit profile of the buyer and ignore the credit of the supplier.

When the sale of a receivable closes, the buyer will be notified. Then on the scheduled maturity date of the invoice, the buyer will owe the investor the full face amount of the invoice. The difference between the buyer's payment to the investor and the investor's discounted payment to the supplier constitutes the investor's fee for participating in the transaction. This is often the only fee that the investor charges; the buyer usually pays no fee on this type of transaction. Also, if the investor is the buyer's cash management bank, the buyer may not have to modify its cash disbursement operations to pay the investor rather than the supplier. In many cases, the investor simply debits a pre-agreed bank account for the amount of each sold receivable on the invoice maturity date.

When the sale of a receivable closes, the buyer will be notified. Then on the scheduled maturity date of the invoice, the buyer will owe the investor the full face amount of the invoice. The difference between the buyer's payment to the investor and the investor's discounted payment to the supplier constitutes the investor's fee for participating in the transaction. This is often the only fee that the investor charges; the buyer usually pays no fee on this type of transaction. Also, if the investor is the buyer's cash management bank, the buyer may not have to modify its cash disbursement operations to pay the investor rather than the supplier. In many cases, the investor simply debits a pre-agreed bank account for the amount of each sold receivable on the invoice maturity date.

Using Negotiable Instruments Instead of Receivables

An open-account vendor-payables program is not the ideal supply chain finance solution for every buyer. Open-account programs rely on the sale of accounts receivable under Article 9 of the Uniform Commercial Code (UCC). The UCC provides an easy and predictable way to finance or sell intangible assets like receivables in the United States. However, in some non-U.S. jurisdictions, selling intangibles can be cumbersome and may expose the investor to additional legal risks, such as risks associated with fraud and insolvency.

Even in the United States, an investor purchasing a receivable needs to record that purchase under the UCC filing system in one or more states. Depending on the supplier's existing credit arrangements, the investor may also need to obtain lien releases from the supplier's lenders before the receivable can be sold.

To bypass these challenges, buyers sometimes opt to implement an alternative structure that utilizes negotiable instruments instead of accounts receivable. A negotiable-instrument–based program is similar in many respects to an open-account program. The supplier submits invoices, which the buyer approves. However, the supplier or buyer also creates a “draft,” a “bill of exchange,” a “negotiable promissory note,” or another form of negotiable instrument. These instruments are governed by U.S. law.

Once created, the instrument is then sold by the supplier to an investor using a process similar to that of open-account receivables sales, but it usually involves a physical embodiment of the negotiable instrument. The investor takes physical possession of the instrument upon purchase, then presents the instrument to the buyer for payment on the invoice maturity date. In some cases, the creation, acceptance, assignment, and presentment of the instrument are handled entirely by the investor, with no need for the supplier and buyer to exchange a physical document.

Because these instruments are governed by U.S. law and owed by a U.S. buyer, they are free of most foreign-law constraints, even if the supplier is a non-U.S. company. Thus, negotiable instruments allow an investor working with a U.S.-based buyer to purchase receivables from a wider universe of suppliers than it could under an open-account program.

The other key advantage of an instrument-based program is what's known as the “holder in due course” doctrine. Section 3-302 of the UCC defines a “holder in due course” as one who takes an instrument for value in good faith, absent any notice that it is overdue, has been dishonored, or is subject to any defense against it or claim to it by any other person. If the purchaser of a negotiable instrument is a holder in due course, the purchaser may not be subject to many of the defenses available to creditors under Article 9 of the UCC. This means that, unlike with open-account programs, invoices sold as negotiable instruments will give the investor priority against claims of the supplier's other creditors, including in a bankruptcy proceeding. Investors should take note, however, that while these programs are built on solid legal foundations, there is little or no case law on the issue of whether an investor in this type of supply chain program would qualify as a holder in due course. In addition, investors often do not need to deal with the UCC recording system when purchasing negotiable instruments.

The other key advantage of an instrument-based program is what's known as the “holder in due course” doctrine. Section 3-302 of the UCC defines a “holder in due course” as one who takes an instrument for value in good faith, absent any notice that it is overdue, has been dishonored, or is subject to any defense against it or claim to it by any other person. If the purchaser of a negotiable instrument is a holder in due course, the purchaser may not be subject to many of the defenses available to creditors under Article 9 of the UCC. This means that, unlike with open-account programs, invoices sold as negotiable instruments will give the investor priority against claims of the supplier's other creditors, including in a bankruptcy proceeding. Investors should take note, however, that while these programs are built on solid legal foundations, there is little or no case law on the issue of whether an investor in this type of supply chain program would qualify as a holder in due course. In addition, investors often do not need to deal with the UCC recording system when purchasing negotiable instruments.

On the other hand, this type of program is more cumbersome than an open-account program and may be unfamiliar to many U.S. suppliers.

Key Considerations in Structured Vendor-Payables Programs

Buyers considering implementing a structured vendor-payables program will want to consider a few key issues. The first, and perhaps the most obvious, is that these programs require close coordination among the buyer's treasury, legal, and purchasing functions. The initial negotiation with prospective investors is usually led by a company's treasury and legal teams, but the purchasing function is generally responsible for on-boarding suppliers and maintaining the program. A lack of coordination among these departments can easily lead to implementation of a suboptimal program and underutilization of the program by the company's suppliers.

The second key issue concerns the accounting treatment of a structured vendor-payables program. For the buyer, the chief accounting priority is usually to avoid having to reclassify the affected payables as short-term indebtedness on its balance sheet. Such reclassification is usually unfavorable because it increases the company's balance sheet leverage, which may affect financial covenants and ratios contained in loan agreements, indentures, and employee compensation agreements, among other contracts.

Unfortunately, no specific U.S. GAAP guidance addresses the accounting for structured vendor-payables arrangements. In 2003 and 2004, Securities and Exchange Commission (SEC) staff made conference presentations outlining general guidance for companies that report to the SEC1. They noted that in specific situations, certain characteristics of structured vendor-payables arrangements may cause supplier payables to be reclassified on the balance sheet of the buyer as short-term indebtedness. Lacking specific GAAP guidance, most auditors use these comments as a guide in making determinations regarding balance sheet treatment.

Auditors are more likely to require indebtedness treatment when a structured vendor-payables arrangement has any of the following characteristics:

- The economic terms and character of the obligations owed to the investor are different from the obligations the buyer previously owed to the supplier.

- The buyer agrees to cover the supplier's financing costs or other obligations to the investor.

- Supplier participation in the program is mandatory.

- The buyer has excessive control in the negotiation of documentation between the supplier and the investor.

Most legal documentation used by sophisticated investors in structured vendor-payables programs is designed to address these concerns. However, buyers should be sure to discuss the implementation of any supply chain finance solution with their internal and external auditors well before they start rolling out a program.

1. SEC Staff Speeches: 2003 and 2004 AICPA National Conference on Current SEC and PCAOB Developments. Robert Comerford: “Classification and disclosure of certain trade accounts payable transactions involving an intermediary.”

An Alternative: Non-Recourse Receivables Purchase

A close relative of structured vendor-payables programs is a non-recourse receivables-purchase solution. This is often described as a “factoring” arrangement, but that's a misleading designation because these facilities have little in common with the small-scale financing mechanism traditionally provided by factoring companies in the United States.

Much like an open-account payables transaction, a receivables-purchase facility entails a supplier selling one or more investors its rights to certain accounts receivable owed by a particular buyer. A big difference is that the buyer's involvement is minimal beyond introducing the investor to its supplier base. The buyer does not have to confirm each invoice before the receivable can be sold. In fact, an investor might provide these types of facilities to suppliers without the buyer even knowing about it. Another benefit for the buyer is that a receivables-purchase facility generally does not have any accounting complications for the buyer.

For suppliers, these facilities can provide much higher advance rates and lower overall costs compared with more traditional asset-based loan facilities. They can also assist suppliers in monetizing excess customer concentrations that would be excluded by the borrowing-base funding formulas found in most asset-based loan (ABL) agreements or accounts receivable securitizations. Traditional ABL and securitization facilities will often contain strict concentration limits on the percentage of receivables of a particular obligor which may be used to generate funding availability. These limits can often be as low as a few percentage points. For many suppliers to industries with a small number of dominant buyers (e.g., retail, auto) these limitations can result in the supplier being unable to monetize a large percentage of its outstanding receivables.

Finally, unlike a structured vendor-payables program, which will usually require a great deal of work at the buyer to implement and roll out among its supplier base, these types of transactions can be executed quickly and sometimes even on a one-off basis.

The downside of these facilities for the investor is that there is no direct confirmation from the buyer that it will pay the investor. Thus, investors in these facilities are very keen to make sure that what they are acquiring from the supplier is a valid and enforceable claim against the buyer. The investor usually conducts significantly more due diligence on suppliers before entering these transactions, and it pays close attention to making sure that the supplier is transferring the receivables via a legal true sale. (See the sidebar Why a “True Sale”?)

The Future of Trade Receivables Monetization

All three of these types of arrangements help suppliers access improved liquidity, whether or not their buyer is looking for extended payment terms. Most of these strategies can be implemented with few, if any, direct expenses to the buyer.

Trade receivables monetization is particularly popular in the consumer retail, automotive and other manufacturing, chemical, and pharmaceutical sectors. Buyers in these industries tend to have extensive supply chains that are global in scope, and generally the buyers are larger, with a more favorable credit profile, than most of their suppliers. However, the benefits of monetizing trade receivables aren't limited to a few business sectors. These strategies may be utilized by any buyer with a solid credit rating and a diverse supplier base, or by any supplier whose buyers have high credit quality.

A lot is happening in supply chain finance, and it seems likely that the recent growth in popularity of these programs will continue well into the future. Based on our own pipeline of projects at Mayer Brown, we expect to be talking about structured trade receivables solutions for a long time. Stay tuned.

————————————————

Massimo Capretta is counsel in Mayer Brown's Chicago office and a member of the firm's banking and finance practice.

Massimo Capretta is counsel in Mayer Brown's Chicago office and a member of the firm's banking and finance practice.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.