The drab world of derivatives clearing, the financial plumbing designed to deliver $400 trillion of annual trades safely, was never supposed to be an emotive issue.

But that depended on regulators preserving the post-2008 spirit of global cooperation. With Brexit inflaming rhetoric between the United Kingdom, United States, and Europe, banks and exchanges are doing their best to prepare for the worst. The risk of the world's financial plumbing breaking down along national lines, triggering extra cost and disruption, is becoming real.

Clearing has become a battleground. A no-deal Brexit doesn't only threaten the ability of London-based firms to seamlessly transact business in the European Union (EU). It could also stop the clearing of trillions of dollars of euro trades on British soil if EU regulators refuse to recognize the U.K.'s rules as adequate.

That might seem draconian, but London's outsized dominance of euro clearing has always rankled on the Continent. Brexit is an opportunity to redress the balance. Doing so could cost firms billions of euros—but the move enjoys political support.

It's unsurprising, then, that Deutsche Bank AG was one of several firms that on Friday announced plans to sell their stakes in London Stock Exchange Group Plc's (LSE's) clearing subsidiary, LCH. Germany's number-one bank is already shifting its primary booking hub to Frankfurt from London, potentially relocating 300 billion euros of its balance sheet. It's possible that the stake in LCH—which could end up unable to clear over-the-counter derivatives for EU firms in a worst-case Brexit—no longer seemed strategic. The sale will also bring in some much-needed cash, but it sends a bigger message that major Eurozone banks have different priorities now.

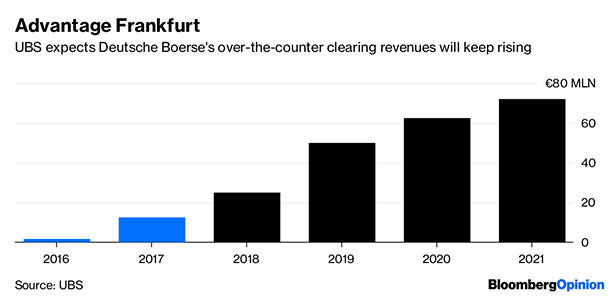

Even before Brexit happens, the clearing business is voting with its feet. LSE's German archrival Deutsche Boerse AG is profiting from this uncertainty. The notional outstanding amount of over-the-counter contracts cleared at Deutsche Boerse surged to 8.4 trillion euros at the end of August, up from 1.8 trillion euros at the end of 2017, according to UBS. The German exchange is stepping up competitive pressure with a new revenue-sharing model, and is determined to win business after several abortive attempts to merge with the LSE. Brexit is an advantage on home ground.

See also:

- Brexit Financial-Market Threat

- Risk of Messy Brexit Mobilizes Corporate Europe and Its Bankers

- Stockpiling Blood and Food

- Brexit Is Reality

Disaster could always be averted. An optimist might view the current situation as a minor, zero-sum game that won't up-end global finance, especially if regulators decide to cooperate for the sake of stability. If the euro clearing market escapes a nightmare scenario of fragmentation, the end result could be a 25 percent market share gain for Deutsche Boerse and a manageable 2 percent to 3 percent hit to LSE's earnings, according to UBS. Cooler regulatory heads could yet prevail.

But the febrile atmosphere isn't helping, and now the U.S. is wading into the fight. Commodity Futures Trading Commission (CFTC) head J. Christopher Giancarlo this week lashed out at European plans to step up oversight of non-EU clearinghouses after Brexit, saying he could not subject U.S. firms to “conflicting or overly burdensome regulation from abroad.” He threatened to block European firms' access to American clearinghouses.

If cross-border financial ties between the U.S., Britain, and Europe are ripped apart by Brexit, the $400 trillion market will never be the same again. Regulators would do well to recapture some of the spirit of unity that followed the 2008 crisis—or risk triggering something worse.

From: Bloomberg

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.