The Federal Reserve raised borrowing costs for the fourth time this year, looking through a stock-market selloff and defying pressure from President Donald Trump to hold off, while dialing back projections for interest rates and economic growth in 2019.

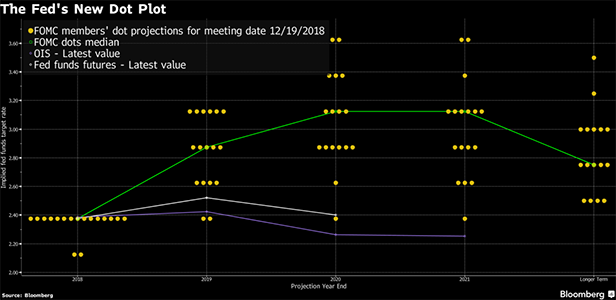

By trimming the number of rate hikes they foresee in 2019 to two, from three, policymakers signaled they may soon pause their monetary tightening campaign. Officials had a median projection of one move in 2020.

Following the Fed decision, stocks erased gains, 10-year Treasury yields fell, and the dollar bounced off its lows of the day. Investors may have been swayed by the Fed's generally upbeat analysis and expectation of more rate increases than markets anticipate.

Chairman Jerome Powell, speaking at a press conference after the decision, stressed that policy was not on a preset course.

“There's significant uncertainty about the—both the path and the ultimate destination of any further rate increases,” Powell told reporters. “Inflation has still remained just a touch below 2 percent. So I do think that gives the committee the ability to be patient in moving forward.”

Powell and his colleagues said “economic activity has been rising at a strong rate,'' according to a statement following the two-day meeting in Washington. While officials said risks to their outlook “are roughly balanced,'' they flagged threats from a softening world economy.

The Federal Open Market Committee (FOMC) “will continue to monitor global economic and financial developments and assess their implications for the economic outlook,” the statement said. The 10-0 decision lifted the federal funds rate target to a range of 2.25 percent to 2.5 percent.

The quarter-point hike came after Trump assailed the Fed on Twitter for two straight days, urging it to hold rates steady in the most public assault on its political independence in decades. Investors are also fretting over the economy, with the S&P 500 Index falling significantly in recent weeks.

Answering questions during the press conference, Powell said political considerations play no role in Fed policymaking. “We're going to do our jobs the way we've always done them,” he said when asked about White House pressure. The Fed will do its analysis and “nothing will cause us to deviate from that,” he added.

Officials also altered key language in their statement, saying the FOMC “judges that some further gradual increases” in rates will likely be needed, a shift from previous language saying the FOMC “expects that further gradual increases” would be required.

In addition, the median estimate among policymakers for the so-called neutral rate in the long run fell to 2.75 percent, from 3 percent in the previous forecasts from September. The median projection is for the benchmark rate to end 2021 at 3.1 percent, down from a prior estimate of 3.4 percent.

Possible Pause

Those are more acknowledgments that rates are moving closer to the point where policymakers will at least take a break from the quarterly procession of hikes they pursued throughout 2018. When taken together, the latest quarter-point move, language changes, and shift in rate projections indicate both continued confidence in the economy and greater caution over how far and fast the Fed expects to move with future hikes. As Powell has said, the Fed is now feeling its way forward and will act in line with how the economy performs.

Investors have had a more pessimistic view than the Fed, foreseeing one increase at most in 2019, according to interest-rate futures prices.

In a related move, the Fed lifted the interest rate it pays on bank reserves deposited at the central bank by just 20 basis points, instead of the usual 25 basis points that would match the quarter-point increase for the fed funds target range. As with a similar move in June, the action was aimed at containing the effective fed funds rate inside the target range.

Careful Balance

Powell is aiming to strike a careful balance, expressing a still-positive view on the U.S. economy without telegraphing a policy outlook that investors might view as too aggressive for an economy that appears somewhat more fragile than just a few months ago. His task is complicated by the repeated attacks from Trump

While job creation has slowed slightly, over the past several months it has still easily outstripped the number needed to accommodate population growth. Unemployment in November remained at 3.7 percent, its lowest since 1969. That has helped lift wages but hasn't provoked any serious signs of excessive inflation.

Still, many forecasters expect growth to slow in 2019 and into 2020, and the Fed's median estimate for gross domestic product expansion in 2019 fell to 2.3 percent from 2.5 percent.

Previous hikes and a stronger dollar will gradually bite into the economy just as fiscal stimulus fades and foreign economies from China to Europe also cool. Meanwhile, the ongoing trade dispute with China and a potentially chaotic exit for the U.K. from the European Union represent significant additional risks.

Financial markets have been turbulent for weeks, with the S&P 500 Index of U.S. stocks dropping 13 percent from the end of September through Tuesday. Yields on 10-year U.S. Treasuries have also been volatile, dropping to 2.82 percent this week after hitting a seven-year high of 3.26 percent in October.

From: Bloomberg

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.