The U.S. Federal Reserve cut its short-term benchmark rate by 50 basis points (bps) on March 3, to a range of 1.0 percent to 1.25 percent, following an off-schedule meeting that caught many market participants by surprise. It was the Fed's first unscheduled cut since the financial crisis. And many analysts expect an additional rate cut at next week's scheduled policy meeting.

Last week's move was uncharacteristically preemptive, designed to buoy markets before the full impact of the coronavirus could be felt on U.S. and global markets. Unlike this cut, reductions in 2008 and after the September 11 attacks in 2001 were reactive. In its commentary issued on March 5, Fidelity Investments explains:

"For policymakers, stepping in early to try to stem further volatility may have been one of the lessons learned from the financial crisis. However, the market reaction to the cut will put the Federal Open Markets Committee (FOMC) in a challenging position, given the already low level of rates. Further rate cuts may be welcome to the financial markets but may not help industries and supply/demand dynamics that are focused on the spread of the coronavirus."

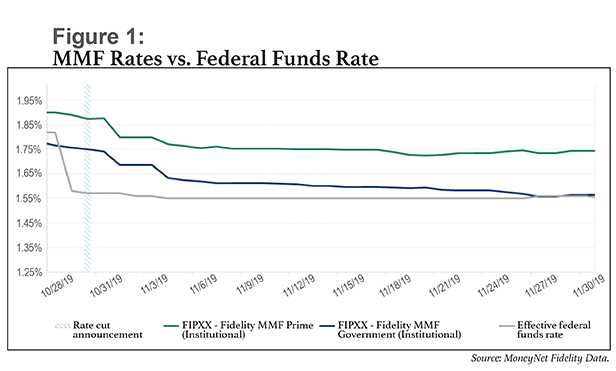

From ICD's vantage point as an independent portal provider for corporate treasury organizations investing in money market funds (MMFs) and short-term instruments, we are seeing clients moving assets away from lower-yielding bank products into money market funds. As the chart below indicates, the impact of FOMC rate reductions on money market fund yields is delayed compared with the federal funds rate.

(See: https://financialintelligence.informa.com/products-and-services/data-analysis-and-tools/imoneynet)

(See: https://financialintelligence.informa.com/products-and-services/data-analysis-and-tools/imoneynet)

ICD CEO Tory Hazard gives this historical perspective:

"With past rate reductions, ICD has seen corporate investors commonly use the opportunity to gain yield in money funds, as there is a lag effect from the fund's weighted average maturity (WAM), generally taking 30 to 45 days to normalize to reduced rates. Supporting this trend in ICI's [Investment Company Institute's] March 5 fund report, institutional money market fund assets increased $20 billion. This increase further validates the perceived safety, security, and liquidity of institutional money market funds in times of market volatility."

This is also the consensus from ICD's discussions with its broad family of fund partners and portfolio managers. One fund partner indicated that institutional investors can look to daily and weekly liquidity for guidance on how quickly prime funds will reset, and commented.

Historically money market funds have experienced inflows during these events, as clients either park cash in money market funds due to a risk-off event or take advantage of the slower reset to new rates. When you consider the 10-year Treasury is now yielding a little over 1 percent, MMFs are very attractive.

Sebastian Ramos is EVP, Global Trading and Products, at ICD. He is responsible for global trading operations, client integration services, and new product introductions. He works closely with ICD's tech team on innovative solutions for the corporate treasury community and has several award-winning solutions and patents to his credit.

Sebastian Ramos is EVP, Global Trading and Products, at ICD. He is responsible for global trading operations, client integration services, and new product introductions. He works closely with ICD's tech team on innovative solutions for the corporate treasury community and has several award-winning solutions and patents to his credit.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.