The U.S. government's main measures of growth in the nation's economy pointed in different directions in the first half of 2022, adding to the ongoing debate around the health of the economy.

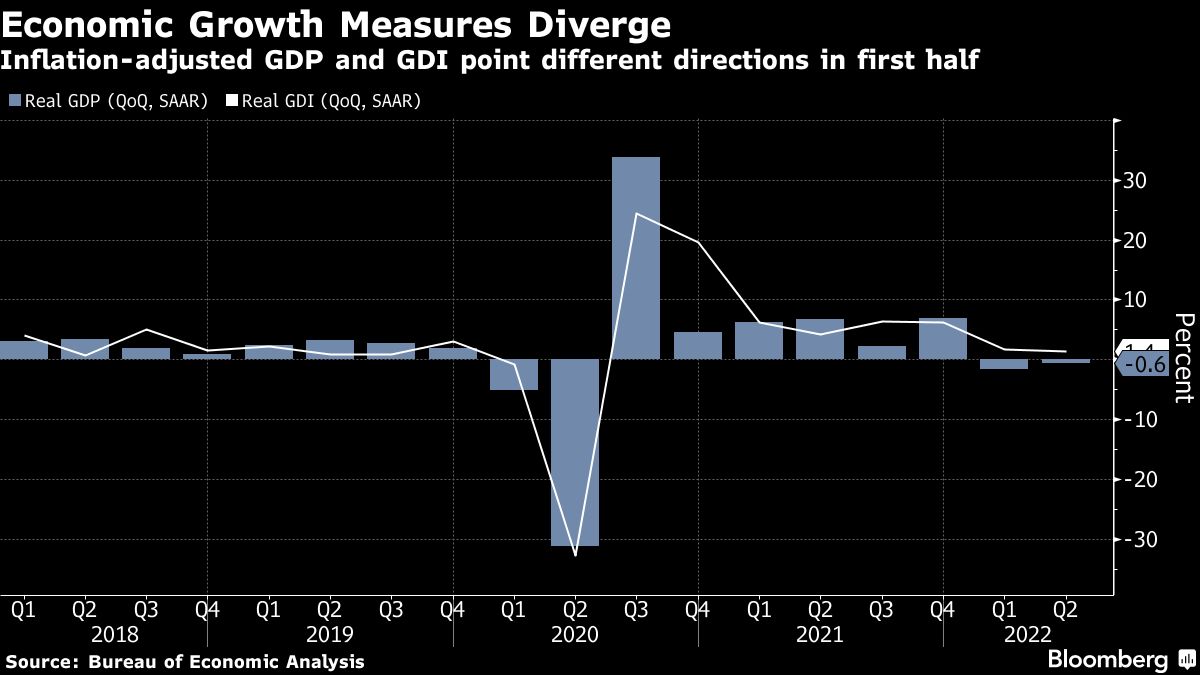

Inflation-adjusted gross domestic product (GDP), or the total value of all goods and services produced in the economy, decreased at a 0.6 percent annualized rate in the April-to-June period, Commerce Department data showed Thursday. That reflects an upward revision in consumer spending; previously, the Commerce Department reported a 0.9 percent contraction.

Recommended For You

However, the other, lesser-known official measure of economic growth—known as gross domestic income (GDI)—climbed at a 1.4 percent rate in the second quarter, after increasing 1.8 percent in the first three months of the year. GDI measures activity by calculating all income generated from producing goods and services, like compensation and company profits.

Theoretically, GDP and GDI should be roughly equal. In reality, they tend to differ, especially in early estimates—but the current gap is particularly large.

The GDP figures suggest an abrupt slowdown in economic momentum in the first half of the year. Under the surface, there's more at play, including the impact of volatile categories like imports and inventories, but overall, consumer spending has decelerated. The occurrence of back-to-back negative quarters, a common rule of thumb for recessions, has not only fueled fears of an imminent downturn, but also led some to believe it was already under way.

GDI, however, points to a more gradual cooling. It paints a picture of an economy supported by a robust labor market and resilient consumer spending, although one that's starting to feel the pinch of the worst inflation in a generation.

See also:

- A CFO's Recession Survival Guide

- Is a 'Soft Landing' Plausible at This Point?

- The New Normal in Liquidity Management

- Economic Indicators Have Gotten Hard to Decipher

Recession Arbiter

The official arbiter of recessions in the United States, the National Bureau of Economic Research's (NBER's) Business Cycle Dating Committee, uses the average of both GDP and GDI, along with a range of other economic variables, when making its recession call. The average of GDP and GDI rose 0.4 percent in the second quarter, after a 0.1 percent increase in the January-to-March period.

"We continue to think that the decline in real GDP across the first two quarters of the year does not meet the NBER's definition of a recession, and if the GDP data are eventually revised up to be more consistent with the GDI data, the first half of the year may end up looking stronger (or at least less weak) than the data currently show," JPMorgan Chase & Co. economist Daniel Silver said in a note.

Separately on Thursday, a report showed applications for U.S. unemployment benefits fell for a second week, suggesting that employers are holding on to workers despite growing economic uncertainty.

Consumer spending, which accounts for the majority of the economy, expanded an upwardly revised 1.5 percent. That compares with a previously reported 1 percent gain.

Thursday's report also included the government's initial estimates of corporate profits in the second quarter. Adjusted pretax corporate profits increased 6.1 percent from the prior quarter—the fastest pace in a year—after falling 2.2 percent in the first three months of the year. Profits are up 8.1 percent from a year earlier.

Inventory and Corporate Profits

Along with consumer spending, private inventory investment was revised higher, though it remained a drag on the headline figure. Residential fixed investment was adjusted lower, the data showed.

Looking ahead, forecasters expect GDP to bounce back in the third quarter, but recession fears remain elevated. The Federal Reserve is aggressively raising interest rates in an effort to cool the economy enough to stem price pressures without causing a recession. So far, the clearest impact for consumers has come in the form of a jump in mortgage rates and ensuing sharp slide in the housing market.

| Categories (SAAR, Quarter-over-Quarter) | 2nd est. | 1st est. |

|---|---|---|

| Real GDP | -0.6% | -0.9% |

| Personal consumption | 1.5% | 1% |

| Nonresidential investment | 0% | -0.1% |

| Residential investment | -16.2% | -14% |

| Exports | 17.6% | 18% |

| Imports | 2.8% | 3.1% |

| Government spending | -1.8% | -1.9% |

Companies have sought to pass the rising cost of materials and labor on to consumers in the form of higher prices, weighing on Americans' ability to spend. Some firms have been able to offset the slip in demand by charging more for their customers, but others, like Target Corp., saw inventories swell, forcing the company to employ steep discounting to clear stockpiles.

While companies report individual profits based on historical costs, the government adjusts the figures to reflect the current cost of replacing capital stock such as equipment and structures. Due to surging inflation, the current replacement costs are much higher.

Excluding that adjustment, as well as one for inventory valuation, after-tax profits climbed 10.4 percent in the second quarter. After-tax profits as a share of gross value added for non-financial corporations, a measure of aggregate profit margins, improved in the period to 15.5 percent—the most since 1950—from 14 percent in the first quarter.

The Bureau of Economic Analysis will release its annual update on September 29, which will include revised statistics for GDP and GDI for the five years through the first quarter of 2022. The first estimate of third-quarter GDP will be released on October 27.

—With assistance from Olivia Rockeman & Matthew Boesler.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.