Passed in 2010, the U.S. Foreign Account Tax Compliance Act (FATCA) is designed to detect offshore banking activities geared toward evading U.S. taxes. The law requires foreign financial institutions and other organizations that accept deposits to identify account holders who may be U.S. taxpayers, then pass on information about those individuals to the IRS so that agency can root out taxes owed. Transactions that involve an undocumented account holder and/or a noncompliant foreign financial institution will be subject to a 30 percent withholding tax.

FATCA will have a large impact on foreign financial institutions. Treasury & Risk sat down with Erick Christensen, vice president and head of the compliance practice at CapGemini, to find out how the law will impact corporate treasurers and other finance managers.

T&R: First of all, what are the impending FATCA deadlines, and who needs to be concerned about them?

Erick Christensen: The first deadlines related to FATCA revolve around getting global intermediary identification numbers (GIINs). Every financial institution that is going to be paying out qualified payments has to sign up with the IRS and get a GIIN that it can present when it goes to settle transactions. It also needs to make sure it's capable of capturing information that comes from correspondent banks. If you're a U.S. bank, most of the work has probably already been done, but if you're a non-U.S. bank or if you're a U.S. bank with foreign subsidiaries, you'll have to get your foreign subsidiaries ready.

T&R: So, only banks have to worry about getting a GIIN?

EC: It's not just banks; it's brokerage firms, it's insurance companies. It's anybody that takes deposits.

T&R: What are the dates for financial institutions around getting a GIIN and registering with the IRS?

EC: July 15, 2013, is when the IRS portal opens and you can apply for this number. The IRS is saying that if you haven't registered by October 25, 2013, you will miss the first publication of GIIN numbers in December. If you miss the first deadline, then you'll start queueing into subsequent time frames. It will start to impact banks pretty dramatically if they can't get this GIIN number in place and start to show it when they settle transactions.

The law also says that on January 1, 2014, financial institutions have to have a new on-boarding system for customers, to identify whether new clients are U.S. taxpayers.

T&R: What are the biggest challenges banks will face in becoming compliant with FATCA?

EC: Well, FATCA is the U.S. regulation, but the implementation of FATCA in foreign countries is being done through what we refer to as intergovernmental agreements, or IGAs. These are agreements that the U.S. Treasury enters into with foreign governments. They take FATCA, the U.S. law, and make it the law of the land in another country. Most countries have privacy laws that prevent financial institutions from sharing client data with a foreign government. Under the IGA, banks provide client information to the local tax authority, and then the local tax authority ships it over to the IRS. This eliminates the privacy law conflict, but there are inconsistencies between the FATCA rules and the IGA rules, so financial institutions have to set up different processes in different countries. A large bank that operates in 50 countries may have 50 separate processes that it'll have to go through to comply with FATCA.

T&R: How will this affect banking customers? Do you anticipate that costs will increase?

EC: Well, some industry analysis has determined that the total cost for global financial institutions to become compliant with FATCA will be almost $1 trillion over 10 years. It's a little too soon to tell whether they will pass those costs on to clients, but someone's going to have to pay for it. For global institutions that operate in 40, 50, 80 countries, becoming completely compliant with FATCA may cost up to $250 million over the next four or five years. In each country, they'll have to do analysis, put processes in place, and be able to report up to the local tax authority. That's a lot of work, and the time frames are relatively short.

T&R: For corporate finance departments, will this mean slower processes when working with banks?

EC: If a bank doesn't use software to automate FATCA compliance—maybe they want to extend out the spend on updating all their systems—the time to on-board new clients is going to get extended. If you currently take 30 days to on-board a new client, including all your AML [anti-money laundering] checks and suitability checks, then adding FATCA checks could increase your on-boarding time to 60 days or 90 days. This could be frustrating for companies because they won't be able to do business with a new financial institution until the on-boarding process is complete.

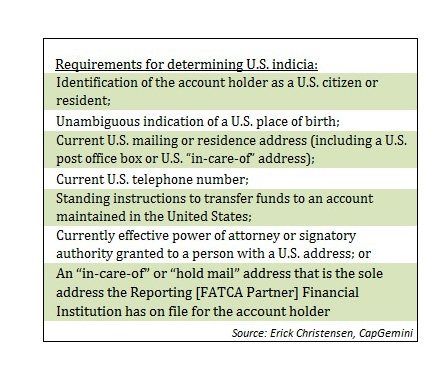

The other piece of this is, if a bank goes through the series of questions it needs to ask new clients and one of the questions triggers a “yes,” then that client has U.S. indicia, meaning the person is potentially a U.S. taxpayer. So then the bank has to go back to the client and say, “Our information shows that you are potentially a U.S. taxpayer. If you are, please certify to us that you are. And if you're not, provide us with the documentation to rebut the presumption that you are a U.S. person.” Banks have to have documentation to show the tax authorities why they made a particular determination on whether a client is or isn't a U.S. person. (See the sidebox “Requirements for determining U.S. indicia.”)

T&R: For a corporate treasurer who's trying to work with a new financial institution, will this translate into a lot more paperwork?

EC: For big, publicly traded companies, it has no impact to at all. The challenge is for smaller entities, where the bank has to pierce through the entity to determine whether there's a controlling investor who might be a U.S. person. The threshold is 10 percent or 25 percent ownership, depending on which country you're in. If an individual owns more than that threshold, the bank has to get information on whether that individual is a U.S. person. Or if there's a company that holds an amount over the threshold, then the bank needs to go to that company and determine whether it has any controlling investors and get information on their U.S. taxpayer status. For a privately held company that is owned by an individual or a family, this can become a very elongated and invasive process.

T&R: Will a company go through this process only once, or will it have to go through the same process every time it works with a new financial institution?

EC: That's a good question. I was in Spain recently, talking to some clients, and one of the things that came up was whether financial institutions can come together and create a database of information about their clients. A lot of them have the same clients, so why does everybody have to replicate the same piece of information over and over? The answer is that privacy laws prevent the sharing of client-level data between financial institutions, although two groups within the same organization can share information. Suppose that Company A is owned by Family B. If Company A opens an account in the wealth area at HSBC and then wants to go open an account in HSBC investment banking, the wealth area can share the company's FATCA information with investment banking. But if Company A goes from HSBC and wants to open an account at RBS, RBS will have to collect all the same data.

T&R: What happens if a company's answers to the questions about U.S. indicia change over time?

EC: Financial institutions have to be notified of any change in circumstance so that they can determine whether they have a U.S. person within the schema and they can figure out whether that triggers an occurrence that is reportable to the tax authorities. For example, one of the questions FATCA asks is: Do you have a U.S. green card? Let's say when a bank does the initial on-boarding of Company A, no one has a green card. But then a member of Family B goes to work in the U.S. and gets a green card. That person becomes a U.S. taxpayer at that point in time.

T&R: In that case, would the company have to go out and proactively notify all its banks?

EC: The way the law is written, the financial institution has to be aware of any changes in circumstances that would change the company's categorization. So the financial institution has to tell clients to notify it if anything changes. Now, if the client lies or withholds something, the bank is not liable for rooting out that information. But if the bank knows about a change—even if the client doesn't mention it—then the bank has an obligation to get that information verified.

T&R: And if you're a finance person, this is something that you're supposed to be doing.

EC: Yes. Suppose you're a finance person in a family-held company that is owned by two brothers. They've always lived in Canada, and each of them owns 50 percent of the company. All of a sudden one brother gets a green card in the U.S.—or buys a condo in Florida so that he has a forwarding address in the U.S., which is one of the indicia of U.S. persons. Once that happens, the corporate finance person would have to go to the company's banks and say, “Hey, we've got a change in circumstance. Brother B has bought a place and now has a forwarding address in the U.S.” That doesn't necessarily mean that he's a U.S. taxpayer now, but the financial institutions have to look into it.

AML is similar. To on-board someone through AML, banks ask a bunch of questions: How much money is going to pass through the account? Where is it going to come from? And if you're going to invest with a brokerage firm, they have to ask you a bunch of questions about your investment suitability, your experience, things like that. FATCA is an extension of where the regulations are going. As a corporate finance person, you have to have that information available to pass on if there's a change of circumstances.

T&R: So, this is where regulations are going?

EC: When FATCA was first announced, no one thought it would ever see the light of day. It was too draconian, too intrusive; it was the U.S. being extra-territorial. They would never be able to enforce it. Well, now it's been enacted, and it's rolling forward. And other tax authorities around the world are starting to see this as an opportunity to capture revenue from their own taxpaying base. Last month, the U.K., Germany, France, Italy, and Spain announced that they are working together to create a sharing of information, and they're patterning it after FATCA and the IGAs. So financial institutions around the globe are going to start asking not just about U.S. persons, but is it a U.K. person? Is it a French person? Is it an Italian? They're going to want more and more information about their clients so that they can pass it on to the appropriate regulatory authorities.

T&R: Ultimately, the finance people in a private company that has several owners around the world will need to keep track of every time they buy a house?

EC: Well, yeah. If you're a privately held company in Canada that does business in the U.S., and an owner of your business buys a home in a third country, all these different tax authorities—which the corporate finance team was not previously engaged around—are going to start asking questions. If you wire money to France to buy a house, you're going to be a client over there, and that financial institution is going to want to know more about your company. Transparency around taxpaying is a huge initiative around the globe right now. Even the secrecy and the privacy that the Swiss have long held are starting to crumble on a daily basis. And it's because of the pressure from tax authorities that are saying, “We need to know, because tax evasion is a huge problem.”

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.