Little has changed in companies' working capital management over the past year—which means that companies have a huge opportunity for improvement. This is the key take-away from this year's “2014 U.S. Working Capital Survey” from REL, a division of The Hackett Group.

Little has changed in companies' working capital management over the past year—which means that companies have a huge opportunity for improvement. This is the key take-away from this year's “2014 U.S. Working Capital Survey” from REL, a division of The Hackett Group.

In this year's iteration of the annual study, REL and CFO Magazine analyzed the 2013 financial statements of the 1,000 largest public companies that have U.S.-based headquarters and are not in the financial services sector (the “REL 1000”). They separated the companies into industry groupings, then organized them into quartiles within each industry in terms of days inventory on hand (DIO), days sales outstanding (DSO), and days payables outstanding (DPO). For every company outside the top quartile in one of these metrics, REL and CFO calculated how much additional cash the organization would have available if it improved efficiency enough in its inventory, accounts receivable, or accounts payable processes to bring the associated metric in line with the level achieved by the top quartile of businesses in its industry.

This analysis revealed that the total opportunity for improving working capital among the 1,000 companies in the study is $1.020 trillion—which separates into a total accounts receivable (A/R) opportunity of $331 billion, a total accounts payable (A/P) opportunity of $266 billion, and a total inventory opportunity of $423 billion.

The study also found that cash on hand increased 12 percent among the REL 1000 from 2012 to 2013, although as a percentage of revenue, cash on hand remained static at 8 percent. Debt also increased, up 8 percent year-over-year and 26 percent over a three-year period. “What we are seeing is that companies are still using the low interest rates, as they have been for the past couple of years, to have access to cash flow,” says Analisa DeHaro, an associate principal in REL's working capital practice. “They've been utilizing the low interest rates to different extents depending on whether they're top performers or in the lower tiers. Now we're looking at how companies are going to fund their capital improvements when interest rates start to rise.”

Balancing Working Capital Tradeoffs

Eventually, when rates increase, companies will have to fund capital expenditures using cash generated through operations. According to the REL/CFO study, the top performers are already doing that by optimizing their working capital management.

“We work with a lot of companies that are looking at the tradeoffs between the different elements of working capital and also costs,” DeHaro says. “They're figuring out which drivers they can actually impact and identifying areas of opportunity. Over the last several years, a lot of companies have been looking to extend payment terms on the supplier side. They've been going through rounds of payment-terms extensions. And now many companies are looking at other ways to improve cash flow.”

“We work with a lot of companies that are looking at the tradeoffs between the different elements of working capital and also costs,” DeHaro says. “They're figuring out which drivers they can actually impact and identifying areas of opportunity. Over the last several years, a lot of companies have been looking to extend payment terms on the supplier side. They've been going through rounds of payment-terms extensions. And now many companies are looking at other ways to improve cash flow.”

Obviously, as companies extend their payment terms on the A/P side, that affects the receivables of their suppliers. “Companies that are being impacted with their own DSO are looking at how they can mitigate that through their own payables,” DeHaro says. “And similarly, if they're looking at expanding inventory, they're figuring out how to make tradeoffs with payables that can mitigate the costs.”

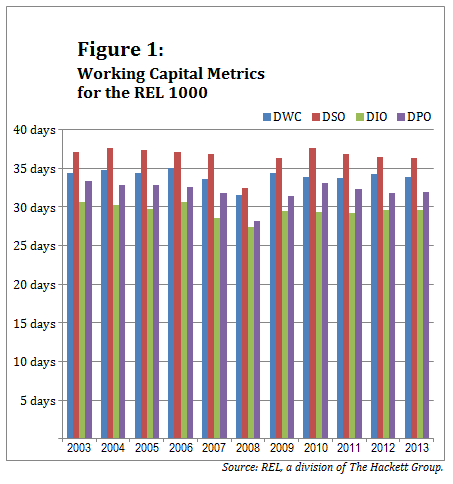

The net result of these calculations, according to the REL/CFO study, is that days working capital—which is trade receivables plus inventory, minus accounts payable, divided by one day's worth of revenue—remained essentially flat in 2013; it fell by 0.3 days, from 34.2 in 2012 to 33.9 in 2013 (see Figure 1, on page 2). But that doesn't mean companies' working capital practices are identical to a year ago.

In fact, the study provides evidence that improvements in one area of working capital management can lead to denigration of working capital performance in other areas. REL and CFO measured the gap in working capital metrics between the organizations identified as top performers and the median company in the REL 1000. In the payables arena, the median company made big strides. DPO for the median organization was 57 percent lower in 2012 than DPO for top performers, but in 2013 this gap fell to just 43 percent. That's the good news. The bad news is that this improvement had serious consequences for the median company's inventory levels. The difference in days inventory on hand between the median organization and top performers increased from 45 percent in 2012 to 59 percent in 2013.

REL views this shift as evidence that organizations which aren't top performers are increasing their payables performance by squeezing suppliers or delaying payments, rather than by implementing best practices. Ultimately, companies that are consistent top performers optimize working capital management on an ongoing basis by implementing processes that routinely balance tradeoffs between receivables, payables, and inventory.

Best-Practice Decision-Making

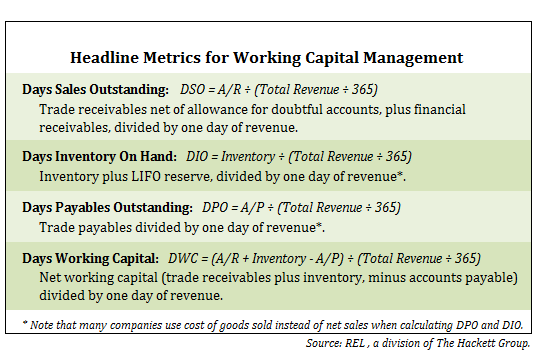

In terms of receivables, DeHaro says, leading companies are undertaking process improvement initiatives in all the different components of the DSO metric (see the sidebar “Headline Metrics for Working Capital Management” on page 3). This is especially true for leading companies in industries where customers are pushing hard for extended payment terms. “DSO is not just terms,” she says. “It is an amalgam of both terms and payment performance. While a company may be getting requests from customers for longer terms, one way it can mitigate that is by having very clear, standardized processes and having lots of tools in place to understand the profitability impacts of offering customers elongated terms.”

Another best practice is to ratchet up credit and collections activities. “Companies need to make sure they're not putting themselves at undue risk in extending credit to their customers,” DeHaro says. “And they need to make collections more effective. Their DSO needs to be more heavily weighted toward the terms that they're negotiating, rather than toward poor payment performance by their customers.”

For inventory metrics, companies should focus on optimizing the levels of inventory they hold. “They need to understand how much they should be holding in buffers or stock,” DeHaro says. “They should evaluate their lead times with suppliers and minimum order quantities.” And the impact of inventory issues on the company's working capital needs to be a routine consideration in procurement decisions. “Companies need to consider all of these factors when they're deciding which suppliers to do business with,” DeHaro adds.

For payables, top-performing companies are evaluating which payment terms are standard in their industry, then they're turning to approaches like dynamic discounting and supply chain finance. “In general, best practices are balancing all these options,” DeHaro says. “They won't necessarily work for all your supplier base, but they'll work for a portion of your supplier base, and you need to determine how they can positively impact your DPO standing.”

The other thing top performers are doing to improve payables performance is automating processes. “They're looking at electronic funds transfer, electronic bill presentment, scanning, those types of technologies, and determining how they can impact their overall payables process, their supplier relationships, and their cash flow,” DeHaro says. “Some are also considering p-cards. All of these things wrap into one another, with tradeoffs between cost and cash flow.”

Integrating Working Capital into Corporate Culture

The top companies are making working capital management a key focus, paying close attention to how net working capital affects their customer relationships and their supply chain. “We are seeing some companies build working capital metrics into their incentives program or their overall goal structure, either for their sales force or across the entire organization,” DeHaro says. Most companies in the lower tiers of working capital performance don't go that far, but they are paying some attention to the tradeoffs inherent in working capital management. “For some companies, the cost take-out may be the priority right now, but it's very rare that we see a company that doesn't have any visibility into at least one of these metrics”—meaning DSO, DPO, and/or DIO, DeHaro says.

According to the REL/CFO study, across all organizations, DSO fell slightly from 36.4 days in 2012 to 36.3 days in 2013; DIO remained steady at 29.6 days; and DPO increased slightly from 31.8 days in 2012 to 32.0 days in 2013. DeHaro attributes the stability of these metrics to the current interest rate environment. She expects that as interest rates rise and cash becomes harder to come by, pressure will mount for companies to move working capital management up the priority list.

According to the REL/CFO study, across all organizations, DSO fell slightly from 36.4 days in 2012 to 36.3 days in 2013; DIO remained steady at 29.6 days; and DPO increased slightly from 31.8 days in 2012 to 32.0 days in 2013. DeHaro attributes the stability of these metrics to the current interest rate environment. She expects that as interest rates rise and cash becomes harder to come by, pressure will mount for companies to move working capital management up the priority list.

A working capital improvement initiative is a major project, but one well worth undertaking. “Working capital doesn't turn around in a month,” she says. “It's something that needs to become part of the corporate culture, part of the incentive program, and part of the company's overall goals and strategies year over year. I think the reason we see the top performers outperforming the median group so significantly may be that these organizations have made working capital management part of their overall standard operating procedure.”

——————–

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

Meg Waters

Meg Waters is the editor in chief of Treasury & Risk. She is the former editor in chief of BPM Magazine and the former managing editor of Business Finance.