When it comes to increasing operational efficiency, fragmentation and manual processes are the enemy. Yet many companies fail to achieve true financial control because they take a fragmented, departmental approach to reconciliation that incorporates multiple systems and frequent manual interventions. Forward-thinking organizations are not only automating reconciliation, but also integrating their reconciliation and attestation processes to provide a single version of the truth based on accurate, real-time, transaction-level data.

When it comes to increasing operational efficiency, fragmentation and manual processes are the enemy. Yet many companies fail to achieve true financial control because they take a fragmented, departmental approach to reconciliation that incorporates multiple systems and frequent manual interventions. Forward-thinking organizations are not only automating reconciliation, but also integrating their reconciliation and attestation processes to provide a single version of the truth based on accurate, real-time, transaction-level data.

Large companies process and reconcile millions of transactions every day, ranging from accruals and accounting (e.g., accounts receivable, accounts payable) to cash deposits and bank reconciliations. These same organizations certify, or attest to, thousands of G/L balances each period. Many of these balance certifications are based on the detailed transaction reconciliations that the treasury and finance teams complete every day.

Fragmented reconciliation systems and processes make it difficult for finance to accurately track and report on accounting information. Any manual work involved in comparing and reconciling data between systems not only increases administrative costs, but also introduces the risk of errors and slows down exception management. If a company can't standardize the exception management process, there's a risk of noncompliance with corporate and industry controls.

One additional pressing challenge is that many companies perform reconciliation checks through systems that rely on only balance-level information. This may help companies identify where exceptions exist—but finding out exactly which transaction caused the discrepancy, and then driving the issue through to resolution, still require extensive manual research.

Any data issues that develop during reconciliation become exacerbated in the company's attestation processes. Once transactions have been stored and reconciled, they are typically passed to a stand-alone system that supports both monthly and quarterly certification of the numbers. To import the right data into the attestation system at the right time, organizations typically take snapshots of balance-level data from the reconciliation system and other systems in which accounting data is stored. This process often relies on manual tools such as spreadsheets, which further increases administrative workloads, costs, and the risk of errors.

Even organizations with more sophisticated stand-alone attestation systems may be exposed to significant risks. This is usually the case when, for example, a company uses a custom-developed attestation system or a non-integrated outsourced service from a third-party provider. Extracts of accounting data may be shared at the file level or may be cut and pasted between systems, providing only a static, point-in-time view. In addition, each system that feeds data into the attestation system may show a slightly different version of the balance sheet. This type of discrepancy can lead to internal discussions about which numbers are accurate, which significantly increases workloads and costs.

Even organizations with more sophisticated stand-alone attestation systems may be exposed to significant risks. This is usually the case when, for example, a company uses a custom-developed attestation system or a non-integrated outsourced service from a third-party provider. Extracts of accounting data may be shared at the file level or may be cut and pasted between systems, providing only a static, point-in-time view. In addition, each system that feeds data into the attestation system may show a slightly different version of the balance sheet. This type of discrepancy can lead to internal discussions about which numbers are accurate, which significantly increases workloads and costs.

Technology for True End-to-End Reconciliation

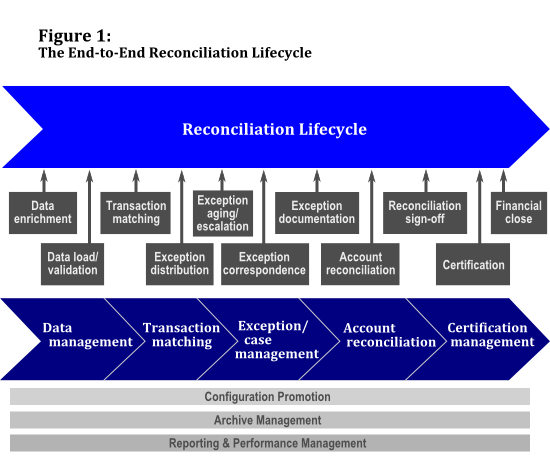

To increase efficiency and reduce financial and regulatory risk, many organizations are deploying technologies that bring reconciliation activities together to present the bigger picture. Figure 1, on page 2 of this article, illustrates the range of different activities that can be pulled into a single system that offers end-to-end reconciliation.

These “true” reconciliation solutions bring transaction-level and balance-level data together in one place, which enables them to provide detailed information on why exceptions have occurred and how they can be resolved. True end-to-end reconciliation solutions provide:

- Support for the full range of transaction types—including wires, checks, cards, ACH, SWIFT transfers, and cash, as well as securities, intercompany transactions, and trades—all in a single system.

- Full automation of the reconciliation lifecycle, from loading and enhancing data to matching, identifying, and solving exceptions, through to certifying the accuracy of the balance sheet.

- Integration of balance-level and transaction-level data to increase visibility into causes of exceptions; eliminate manual interventions; and provide rapid, cost-effective resolutions.

- Standardization of processes for transparency and visibility across all transaction types and scenarios.

- Enforcement of enterprise-wide governance and controls, including the critical period-end close process.

Benefits abound for companies that bring all these activities into a single system. Elimination of manual research or interventions at any stage of the process enables the company to free up staff for more value-added work, such as identifying root causes of exceptions and trends in the data. It can also bring major reductions in per-transaction costs.

At the same time, end-to-end reconciliation streamlines accounting and reporting processes and improves the management team's visibility of business performance. Payments made late in the month, for example, are captured centrally in real time, ensuring that accounts can be closed more quickly and accurately. Meanwhile, a true reconciliation system dramatically reduces the risk of error that arises when people are frequently rekeying data across multiple systems.

Centralize to Optimize

Despite the benefits of automation, some companies are daunted by the idea of stripping out legacy systems and automating a wide range of previously manual administrative tasks. Many organizations have found that centralizing reconciliation based on a center of excellence (COE) or shared-services delivery model can help kick-start the improvement process. Centralization of reconciliation processes provides major benefits that mirror those of technology-powered process automation. Centralization can reduce costs, liberate staff to spend time on more value-added activities, and provide senior management with better visibility, as centralization releases information previously held in siloed systems for a current, accurate view of business performance.

Before embarking on a shared-services or COE strategy, however, a company needs to look at its current reconciliation systems and processes and define exactly what it wants to achieve in the future. It should bring together reconciliation specialists from across the business to define and clearly state the company's objectives in centralizing reconciliation; goals could include improving visibility into enterprise controls, adopting sustainable risk mitigation and compliance practices, reducing processing costs, and increasing efficiency. Whatever strategic direction the project team settles on, they must make sure that senior management is on board. The shift to a centralized model means bringing multiple reconciliation teams and resources into a single, cohesive function. This requires significant reorganization, as well as investments in infrastructure and training, so support from top-level management is crucial.

Once the project team has determined the goals and objectives of the centralization and/or automation initiative, they need to establish consistent reconciliation rules and define those rules using comprehensive process templates. The same group also needs to decide which elements of the process should be included in the shared-service center or COE. Decisions should be based on a detailed assessment of each element of the process and its value for the business.

Once the project team has determined the goals and objectives of the centralization and/or automation initiative, they need to establish consistent reconciliation rules and define those rules using comprehensive process templates. The same group also needs to decide which elements of the process should be included in the shared-service center or COE. Decisions should be based on a detailed assessment of each element of the process and its value for the business.

One common mistake is to think of the shared-services function as another siloed department, but this limits its value. Building bridges with all departments and keeping the lines of communication open are the routes through which the shared-service center can identify new opportunities for process improvements and collectively agree on changes that add value for internal customers.

All these decisions lay the groundwork for the drafting of a project plan. The best approach is a phased implementation, in order to introduce employees to the new process in stages. This enables the project manager to plan for capacity growth over time and to incrementally invest in skills and technology that will result in broader benefits. A shared-services approach reduces costs in the long term, but it can increase the short-term investment required to bring an automation solution to fruition.

In planning the phased implementation, the company should identify high-value lines of business—those that are likely to reap big benefits from automation—and roll out to these groups first, because an early demonstration of value is critical to long-term success across the company. Then, as use of the shared-services or COE model expands, the project team must make sure to establish clear lines of communication. As the shared-services plan starts to gain the trust and support of different business lines, it may be prudent to reinforce that support by demonstrating the value of shared services back to the business. This can be done by quantifying costs per transaction and return on investment, engaging new areas of the business, and improving service-level agreements.

When organizations reach advanced stages of maturity, the shared-services model begins to deliver quantifiable value. Performance measures can be used to effect major process improvements, and to establish the shared-service function as a trusted adviser and partner to all departments and business lines across the company. Whether the shared-services function resides inside or outside the organization, a standard charging model should be implemented based on per-transaction billing or billing over a specific time period. This makes it possible to quantify return on investment, engage new areas of the business, and increase adoption for services.

Fragmentation is the enemy of solid controls—whether it is fragmentation in the reconciliation lifecycle, utilizing different solutions for reconciling data and performing the period-end close, or fragmentation in the process itself. Centralization and a shared-service model enable a company to effectively tackle reconciliation across the organization in a consistent, timely, and predictable manner.

————————————–

Eric Werab is director of product portfolio management for Financial Control Solutions at Fiserv. He is responsible for the strategic direction of the company's suite of reconciliation and financial control products. In this capacity, he works with customers across many markets to understand their internal-control needs and ensure the Fiserv solutions meet these needs.

Eric Werab is director of product portfolio management for Financial Control Solutions at Fiserv. He is responsible for the strategic direction of the company's suite of reconciliation and financial control products. In this capacity, he works with customers across many markets to understand their internal-control needs and ensure the Fiserv solutions meet these needs.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.