It's no secret that businesses around the world have been hoarding cash since the Great Recession. On the surface, this makes sense. Money in the bank is readily available when it's needed for investments, and it can serve as a financial buffer should hard times hit again. However, many companies accumulate cash by squeezing their suppliers—a practice that a recent survey suggests may undermine the stability of the economy overall.

It's no secret that businesses around the world have been hoarding cash since the Great Recession. On the surface, this makes sense. Money in the bank is readily available when it's needed for investments, and it can serve as a financial buffer should hard times hit again. However, many companies accumulate cash by squeezing their suppliers—a practice that a recent survey suggests may undermine the stability of the economy overall.

The study was completed by MasterCard and e-invoicing provider Basware. It polled 1,015 finance decision-makers with a view of both accounts receivable and accounts payable. Respondents were distributed roughly equally across 10 countries, including the U.S., Australia, the U.K., Germany, and six other European nations.

Among these respondents, almost half (48 percent) said their company has more cash in the bank today than it had a year ago. Only 11 percent said their company's cash position has weakened in the past year. Businesses that are cash-rich have used a variety of tools to reach that state.

Recommended For You

More than two in five respondents (41 percent) said their company has accessed credit/financing during the past year. Thirty-five percent have tapped into an asset-based loan, and 34 percent have leveraged supply-chain finance. Thirty-seven percent said their company has engaged in dynamic discounting, and 35 percent have used factoring. Meanwhile, 44 percent said their organization has tightened payment terms for buyers. But the flip side of the payment terms equation—delaying payments to suppliers—is by far the survey's most frequently cited method for increasing cash reserves.

More than half of respondents (57 percent) said that over the past year their company has delayed payments. This statistic concerns Esa Tihilä, CEO of Basware, and Hany Fam, president of MasterCard Enterprise Partnerships, whose companies have partnered to incorporate payment capabilities into a broad electronic invoicing network. "If a buyer is not paying his bills on time, he's causing trouble for his suppliers," Tihilä says. "When this practice becomes widespread, it can have an impact on the whole economy. And we are seeing that now, in different countries. In the European Union, more than half of the economy is made up of small to midsize businesses. When these companies are paid late, that causes a cash flow issue. And we are seeing pretty significant effects in Europe.

"The level of predictability around a company's accounts receivable has a direct impact on the business's risk-taking behavior," Tihilä adds. "When you have predictability in your cash flow, you are able to take risks and to make larger decisions, because you can count on what money is coming in, and when. On a larger scale, lack of predictability affects employment and affects consumption, which can have a huge impact on the whole economy."

One of the survey's more interesting findings may be that 88 percent of all survey respondents—and 97 percent of respondents from the United States—believe that companies have a "social responsibility" to pay their suppliers on time. Globally, 40 percent of respondents believe that persistent late payment of invoices limits the flow of funds between employers and workers, 31 percent think it limits growth in the economy, and 13 percent believe it reduces employment. Survey respondents also see late payments as limiting the flow of funds between buyers and sellers (45 percent) and between companies and investors (37 percent). One in five (21 percent) believe it also increases taxes.

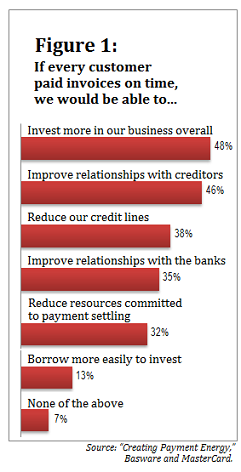

Many of these expectations are logical assumptions, considering that nearly half of the finance decision-makers who participated in the survey said their company would invest more in its business if every customer paid its invoices on time. And 35 percent said eliminating late customer payments would improve their own relationships with their banks. (See Figure 1.)

Many of these expectations are logical assumptions, considering that nearly half of the finance decision-makers who participated in the survey said their company would invest more in its business if every customer paid its invoices on time. And 35 percent said eliminating late customer payments would improve their own relationships with their banks. (See Figure 1.)

Nevertheless, 67 percent of all survey respondents, and 77 percent of those from the United States, admitted that their company has used payment terms as a strategic lever to help manage its cash flow during the past year. Nearly three-quarters indicated that they think late payment is an unavoidable fact of business life (72 percent of respondents from the U.S. and 74 percent overall).

"People agree that payments should be made on time," MasterCard's Fam says. "But they're nervous, so they're using late payments as a means of cash flow management in times of uncertainty. In some cases, they're incapable of paying on time because they don't have adequate insight into their own cash flow coming in from people they're expecting payments from." It's a vicious cycle, and one that Basware and MasterCard have set out to break.

"Lumpy cash flows are a function of lumpy orders and invoices," Fam says. "And lumpy orders and invoices are a function of uncertainty in corporations. If companies can interact and transact and purchase and pay in a more consistent, stable fashion, that will have a positive effect on transparency of operations, predictability for the business, and even on the overall economy."

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.