We live in a globalized world, where expanding overseas is considered the new normal for ambitious companies. Indeed, since 2010, North American businesses' mergers with and acquisitions of European organizations have totaled 3,979 transactions, worth a sum of US$506 billion, according to Dealogic.

We live in a globalized world, where expanding overseas is considered the new normal for ambitious companies. Indeed, since 2010, North American businesses' mergers with and acquisitions of European organizations have totaled 3,979 transactions, worth a sum of US$506 billion, according to Dealogic.

For multi-billion-dollar institutions, growth by international merger or acquisition is a relatively simple process. Many of the Fortune 500 have at their disposal shared service centers for an assortment of financial activities, so the operational integration of a new market into the existing payments management structure is relatively straightforward. However, cross-border payment issues often create challenges for midsize companies.

Despite the introduction of the Single European Payments Area (SEPA), North American mid-cap organizations taking advantage of growth opportunities in Eastern, Central, or Western Europe face complex and diverse payment considerations. Stumbling blocks in creating a trans-Atlantic footprint can arise from the environment's alien regulations, multiple tax jurisdictions, conflicting capital management rules, and varying degrees of political stability within and outside of the Eurozone—not to mention the more obvious challenges of varying time zones, languages, and currency risks.

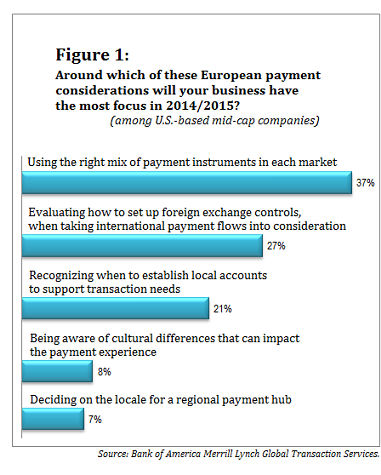

Bank of America Merrill Lynch recently surveyed 61 of our U.S.-based mid-cap corporate clients, and we found that their five largest payments challenges in Europe are using the right mix of payment instruments, setting up foreign exchange (FX) controls, recognizing when they need local accounts to support transactional activities, understanding cultural differences that can impact the payment experience, and selecting a locale for a regional payment hub. (See Figure 1, below.)

Despite the developed trade relationships many U.S. corporates share with European nations, the Continent is vastly different from the U.S. market. What underpins this differentiation is cultural compatibility: Integrating a company's treasury and liquidity management systems is as much a human exercise as it is financial. If the key priorities for U.S. mid-caps expanding into Europe are to balance different payment instruments, manage localized operations, and implement multiple FX controls in each market, what are the options and what are the key components of this Euro-American “culture shock”?

Checking out or Cashing In?

For the North American treasurer, checks are commonplace, whereas in Europe the past few years have witnessed a rapid decline in the use of paper checks, as card and ACH payments have experienced an exponential rise in popularity. The volume of transactions completed in Europe via check fell from just over 5 billion in 2010 to 3.7 billion in 2013. This meant that checks constituted just 3.7 percent of all transactions administered, and they declined by more than any other payment instrument during the three-year period.1 But their decline is not happening consistently across all of Europe. In the Netherlands, checks have not been used for several years. At the same time, in countries such as France and Ireland, checks still constitute around 10 percent of all transactions.2

Moreover, although paper payments are increasingly being replaced by electronic invoicing, many European firms continue to pay support staff in cash. This trend comes with a certain level of risk for a foreign acquirer. Cross-border payments require accountability, but holding petty funds in cash opens a company to fraud and human error, both of which impact the accuracy of cash flow reporting. We expect to see continued reduction in the use of cash in the near future, and we have already witnessed ATM withdrawals across Europe, as a percentage of all transactions, decreasing from 13.6 percent to 9.6 percent between 2010 and 2012.3

The competition to be Europe's most popular payments instrument has become a three-horse race. In 2013, cards accounted for 43.6 percent of transactions in Europe, whilst credit transfers accounted for 26.5 percent and direct debits constituted 23.9 percent of all European transactions.4 In certain European countries, the ACH payments process has undergone extensive changes that bring the Continent closer to the American way of doing things. In ACH, as in other areas, the diversity of the payments landscape among European countries means the level of culture shock can vary significantly for corporate treasurers entering different European markets.

It's important for companies growing through cross-border acquisition of new customers, suppliers, or business units to understand the payment tools at their disposal. Some of those tools are uncommon in the United States. And although checks are very familiar in the United States, treasury departments doing business in Europe should not consider checks their payment method of choice. Electronic instruments that are used widely in Europe—such as wires or ACH transactions—will often suffice, and they require far less manual processing than a check payment, carry less risk of fraud, and entail less delay from a float perspective.

It's important for companies growing through cross-border acquisition of new customers, suppliers, or business units to understand the payment tools at their disposal. Some of those tools are uncommon in the United States. And although checks are very familiar in the United States, treasury departments doing business in Europe should not consider checks their payment method of choice. Electronic instruments that are used widely in Europe—such as wires or ACH transactions—will often suffice, and they require far less manual processing than a check payment, carry less risk of fraud, and entail less delay from a float perspective.

For transactions that are not urgent, treasurers should consider low-value electronic payment methods, such as BACS in the United Kingdom and SEPA credit transfers for euro-denominated payments. These payment methods are much cheaper than wire transfers, and when they're used for known payments such as payroll or taxes, the treasury team can manage around their two- or three-day settlement cycle. Also, if a treasurer needs to make an urgent low-value payment in the U.K. (less than £100,000), Faster Payments is effectively a same-day ACH payment that can be used instead of an expensive wire.

Direct debits are another helpful tool, although in many cases they're more suited to collections than to payments. Direct debits allow a creditor to take money from a debtor's account on a pre-agreed day, greatly helping the creditor with its cash forecasting and working capital management. We always recommend talking to your banking partners to understand which instruments are available, and when each makes the most sense to use.

Going Global by Staying Local

With the introduction of SEPA, the local nuances in treasury practices across Europe have narrowed. Thus, on the face of it, the regulation appears to have removed a company's need to maintain individual accounts across Europe. In reality, however, going global often requires staying local. It's true that the transmittance of ACH lends itself to centralized-account payments via SEPA. But the need for petty cash; routine, low-value check issuance; and capital restrictions mean that local bank accounts remain a necessity in some countries.

SEPA continues to be implemented in different ways in different nations. For example, account opening and reporting requirements in Cyprus, Italy, and Sweden require localized payment methods. Such is the nature of the Euro-American “culture shock.”

Another treasury issue that companies must consider before doing business in a new geography is what software system they will use to execute and report on transactions. In Europe, local offices often use an online treasury workstation to input transaction instructions, to simplify payment authorization by a regional hub or head office. Third-party software platforms are favorable for high-value, single-currency payments, whilst bank systems tend to cater to low-value, multicurrency transactions, which they automate and standardize against U.S. reporting requirements.

3. ECB Payments Statistics [23 August 2013]

4. ECB Payments Statistics [23 August 2013]

For companies considering establishing a shared service center to handle European payments, the U.K., Ireland, Luxembourg, the Netherlands, Germany, and Switzerland are usually key regional pins on the European payments map. Each specializes in operating payment hubs for certain industries, and together these countries comprise the European economic powerhouse. But with increasing volatility across the Continent, new locations for shared service centers are appearing. The Czech Republic and Poland forecast 2015 GDP growth of 2.4 percent and 3.5 percent, respectively.5 These numbers may convince some mid-caps to locate their payment hubs in the geographies that are exposed to the highest growth in trade and consumption.

It's also important to understand that trade flows are much more diversified in Central and Eastern Europe than in the United States. This impacts not only the strategic location of a company's banking services, but also the cash management choices available to a U.S. mid-cap. Variations in levels of incentives, denomination in euro or British pound, and labor costs all mean that there is no one-size-fits-all global treasury solution across a continent characterized by change.

One important difference that treasurers need to take into consideration is that different countries and industries have different methods and cultures around paying employees. For example, in Italy many companies are comfortable paying employees with forward-dated checks. Some countries and industries prefer using cash, while others favor payroll systems.

One important difference that treasurers need to take into consideration is that different countries and industries have different methods and cultures around paying employees. For example, in Italy many companies are comfortable paying employees with forward-dated checks. Some countries and industries prefer using cash, while others favor payroll systems.

Managing Growth

Expanding supply chains across the pond creates expected currency risks, and it's up to the treasury team to manage those risks. For mid-cap companies, whose treasury managers may not have any expertise outside of dollar-denominated cash management, repatriating funds from Europe is often the largest payments consideration. When it comes to handling local funding requirements in different European countries, or determining the denomination of an invoice for an overseas buyer or supplier, there is no magic bullet.

As a rule of thumb, transactions are typically denominated in the supplier's currency, but this may change when the businesses have a significant difference in size. For example, a small supplier selling to a very large buyer may have no choice but to issue an invoice in the buyer's currency because it may be specified in the terms of trade. The result of this arrangement is that the supplier risks losing a handle on its margin due to fluctuating currency prices, and it may need to consider a FX hedging strategy to protect them from this exposure.

That said, there may be an opportunity to build in a buffer to the invoice price to help protect the supplier from currency fluctuations. Equally, a small, specialist supplier to a large buyer may be in a position to dictate terms because it may be in the “driver's seat” from a supply-and-demand standpoint.

Minimizing the Culture Shock

Strategic change will undoubtedly create upheaval. Growth by acquisition presents the treasurer with a variety of challenges, many of which are peculiar to individual payment jurisdictions. Regulatory changes under SEPA have prompted a shift toward a more universal payments system akin to that of the U.S., but the pace of change varies across Europe.

The balance of payment instruments, alignment of local treasury requirements within a global payments structure, and management of growth via FX controls are all underpinned by a common denominator: cultural compatibility. The degree of “culture shock” for the U.S. mid-cap expanding operations overseas can be somewhat mitigated by fully understanding the breadth of payment considerations across the Continent.

5. World Bank Global Economic Prospects database [Access: 07/01/2015]

——————————————-

Alex Weaving is head of commercial sales for Global Transaction Services, EMEA at Bank of America Merrill Lynch. He manages the team responsible for selling the full breadth of the company's Global Transaction Services product set to EMEA commercial clients including cash management, trade services, trade finance, and commercial cards.

Alex Weaving is head of commercial sales for Global Transaction Services, EMEA at Bank of America Merrill Lynch. He manages the team responsible for selling the full breadth of the company's Global Transaction Services product set to EMEA commercial clients including cash management, trade services, trade finance, and commercial cards.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.