Eight years after the beginning of the financial crisis, regulators and financiers are still searching for the optimal balance between encouraging global growth and implementing regulations on trade finance instruments that are adequate, equitable, and risk-aligned.

Eight years after the beginning of the financial crisis, regulators and financiers are still searching for the optimal balance between encouraging global growth and implementing regulations on trade finance instruments that are adequate, equitable, and risk-aligned.

This is a crucial discussion, especially for developing nations and the companies looking to do business there. Trade finance assists buyers and sellers by filling in the trade cycle funding gap and removing the payment risk and supply risk. It is therefore a key factor in emerging-market development, as governments and regulators around the world recognize.

The International Chamber of Commerce's (ICC's) Trade Register report presents a global view of the credit risk profiles of trade and export finance transactions, focusing on credit-related default and loss experience. This encompasses short-term products, which typically have a maturity of less than one year, such as issued import letters of credit (L/Cs), confirmed export L/Cs, import and export loans, and performance guarantees and standby L/Cs. The scope of medium- to long-term trade finance products is limited to products where an OECD Export Credit Agency (ECA) has provided a state-backed guarantee or insurance to the trade finance bank.

Trade finance is critical to the expansion of trade. Without it, trade remains constrained, impacting economic development and increasing instability across all sectors, countries, and populations. Yet global banks have been reducing their counterparty networks in the developing world, and thus reducing the amount of trade finance available in this region.

There are many reasons behind the withdrawal of global banks from the emerging markets. One is the high cost of compliance and due diligence incurred when operating in this area. Another is the global regulatory climate, including the capital requirements imposed by Basel III, which reduce the amount of lending a bank can offer at each level of capital reserves it has on hand. What's more, anti-money laundering (AML) and know-your-customer (KYC) requirements, although essential, have weighed banks down with new investigative, tracking, and reporting responsibilities.

Bank de-leveraging and tighter global credit conditions—driven in part by financial, regulatory, economic, and political considerations—pose a serious challenge to trade growth.

Growing Trade Finance Gap

Industry sources estimate that the average cost of maintaining a basic correspondent banking relationship has increased at least five times since the peak of the financial crisis. Indeed, in ICC's 2015 Global Survey on Trade Finance report—which collates feedback on the timing and calibration of reforms, and includes full industry representation and coverage—46 percent of banks reported termination of relationships, due at least in part to the added cost or complexity of those relationships' maintenance.

This has significant repercussions on emerging markets, which are dependent on trade finance as an engine for growth. Small to midsize enterprises (SMEs), in particular, experience higher levels of unmet demand for trade finance, for a variety of reasons ranging from risk profile to issues of bankability and the need for significant advisory support. The termination of correspondent banking relationships denies emerging markets access to global supply chains and trade corridors, as well as access to liquidity they need for growth and expansion. Considering that emerging markets continue to take on an increasingly larger share of global trade, and account for around 42 percent of global exports, a lack of trade financing clearly slows global growth rates.

This has significant repercussions on emerging markets, which are dependent on trade finance as an engine for growth. Small to midsize enterprises (SMEs), in particular, experience higher levels of unmet demand for trade finance, for a variety of reasons ranging from risk profile to issues of bankability and the need for significant advisory support. The termination of correspondent banking relationships denies emerging markets access to global supply chains and trade corridors, as well as access to liquidity they need for growth and expansion. Considering that emerging markets continue to take on an increasingly larger share of global trade, and account for around 42 percent of global exports, a lack of trade financing clearly slows global growth rates.

The ICC survey also suggests that the trade finance gap may be increasing. Fifty-three percent of respondents perceive a shortfall between banking customers' demand for trade finance and their ability to satisfy that demand. Closing this gap requires continuing collaboration between trade banks and other private sector sources, together with ECAs and multilateral development banks—both groups critical to ensuring adequate availability of trade financing. Additionally, industry stakeholders have recognized the need to attract non-bank capital in support of trade finance, and measures are being taken to better communicate to investment-pool managers about the nature of trade finance.

Advocacy and collaboration on the regulatory side, based in part on the ICC Trade Register data, underpin ongoing efforts to find the right balance between the need for growth-driven trade (enabled by trade finance) and the need for appropriate, risk-aligned capital adequacy and compliance regulation. Ultimately, this has freed up bank balance sheet capacity to underwrite more trade finance business. As illustrated in the Trade Register report, there have been several substantive successes to date, though it is clear that continuing engagement with the Basel Committee, along with regional and national regulatory authorities, is necessary on this front.

Advocacy and collaboration on the regulatory side, based in part on the ICC Trade Register data, underpin ongoing efforts to find the right balance between the need for growth-driven trade (enabled by trade finance) and the need for appropriate, risk-aligned capital adequacy and compliance regulation. Ultimately, this has freed up bank balance sheet capacity to underwrite more trade finance business. As illustrated in the Trade Register report, there have been several substantive successes to date, though it is clear that continuing engagement with the Basel Committee, along with regional and national regulatory authorities, is necessary on this front.

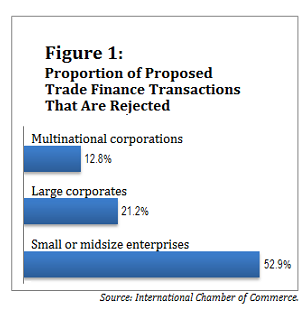

SMEs in riskier markets bear the brunt of the trade finance gap. These businesses account for 46 percent of proposed trade finance transactions, but only 47 percent of these transactions are accepted; more than half are rejected. By comparison, 79 percent of trade finance transactions for larger corporates are accepted. (See Figure 1.) This gap has a significant impact on global development; the Asian Development Bank estimates that unmet demand for trade finance around the world, among companies of all sizes, amounts to US$1.1 trillion.

Trade Finance Is Low-Risk

Although the trade finance gap clearly persists, there is reason for optimism. In the ICC Global Survey on Trade Finance, 61 percent of respondent banks reported increases in their capacity to meet trade finance demand. A key reason behind this positive trend is that banks are becoming increasingly aware of the importance, and very effective mitigation, of the risks inherent in trade finance.

Indeed, in the latest edition of ICC's Trade Register, traditional trade finance products fare particularly well, both at the customer and transactional level, and when weighted by exposure. For example, the transaction default rate for short-term export L/Cs was 0.01 percent between 2008 and 2014, which corresponds to a Moody's rating between Aaa and Aa. Figures for medium- to long-term trade finance products are also positive, with an annual loss rate from 2007 to 2014 that is lower than the loss rate reported by Moody's for Aa-rated bonds. In fact, the corporate default rate of 0.88 percent for medium- to long-term trade finance products, across all asset classes, compares very favorably with the Moody's default rate of 1.9 percent for all rated corporates.

And even in the event of default, trade finance instruments record high rates of eventual asset recovery. The median result for all short-term trade finance products is close to 100 percent recovery. Even with prudent assumptions, the average expected loss for short-term trade finance is lower for all products than that of typical corporate exposures.

Open and Constructive Dialogue Around Trade Finance

The results of the 2015 Trade Register analysis remain broadly consistent with findings over the last seven years, since the inception of the Trade Register, and continue to provide a sound and objective basis for constructive, substantive dialogue and advocacy with the Basel Committee and other regulatory authorities. Even as we all recognize the need for regulatory oversight aimed at assuring a robust global financial system, it is clear that trade finance products should be treated as low-risk credit instruments.

Of course, opportunities to further balance regulatory objectives with trade finance value creation remain, and extend to compliance and regulatory issues beyond the capital adequacy discussion. For instance, trade-based money laundering, which drives certain types of financial-sector regulation, must be further explored, considering that only a small portion of such activity actually occurs in the context of trade finance transactions.

In particular, there is room for greater communication and understanding among bankers, trade financiers, and other stakeholders so that all parties strive to reach informed decisions about the best way forward. As such, the improved tone, approach, and substance of dialogue are all to the good, and must continue.

In particular, there is room for greater communication and understanding among bankers, trade financiers, and other stakeholders so that all parties strive to reach informed decisions about the best way forward. As such, the improved tone, approach, and substance of dialogue are all to the good, and must continue.

The next phase of the dialogue and advocacy work can very usefully extend to involving representatives from the client community of users of trade financing—from treasury and finance executives in large multinationals, to entrepreneurs leading economically critical small businesses. The matter of availability of trade finance and appropriately risk-aligned regulation of this business are not fundamentally “bank problems,” but issues of importance to trade flows and real economic activity.

Companies of all sizes can engage in this dialogue and advocacy effort through various channels, from industry associations to chambers of commerce, to numerous international and multilateral institutions active in the financing of international trade and related advocacy efforts—which today extend from the ICC to the Basel Committee, the World Trade Organization, the B-20/G-20 annual processes, the United Nations system, the World Economic Forum, and numerous other organizations.

A concrete first step may be for treasurers to reach out to their trade financers or to organizations like the ICC Banking Commission, BAFT in Washington, and others to share their views and experiences, and ultimately to contribute to shaping policy in this area.

The importance of engaging companies and private-sector end clients in this process increases as we shift our attention from traditional trade finance mechanisms and instruments to the increasingly crucial and fast-growing area of supply chain finance, which takes a holistic, ecosystem-level view of trading relationships and involves multiple commercial relationships—sometimes supplier communities numbering thousands—touching multinationals as well as micro-enterprises and SMEs, often located in developing economies.

——————————————————

Alexander R. Malaket, CITP, is the deputy head of the executive committee for the International Chamber of Commerce (ICC) Banking Commission and president of OPUS Advisory Services. He has over 25 years of professional experience in trade, trade finance, investment, financial services, and senior-level consulting.

Alexander R. Malaket, CITP, is the deputy head of the executive committee for the International Chamber of Commerce (ICC) Banking Commission and president of OPUS Advisory Services. He has over 25 years of professional experience in trade, trade finance, investment, financial services, and senior-level consulting.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.