The world's biggest bond market may have finally broken out of its tight 2017 trading range, but it's not exactly drawing a clear roadmap for traders of the moves ahead.

Rather than gaining more insight into the plight of the global reflation bet, traders were left reacting to geopolitical risks from North Korea to Russia (not to mention a huge bomb dropped in Afghanistan just before holiday-shortened trading ended). They also heard President Donald Trump jawboning the dollar lower and declaring he likes low interest rates now that he's in the Oval Office. Those factors seem unlikely to disappear in the weeks ahead.

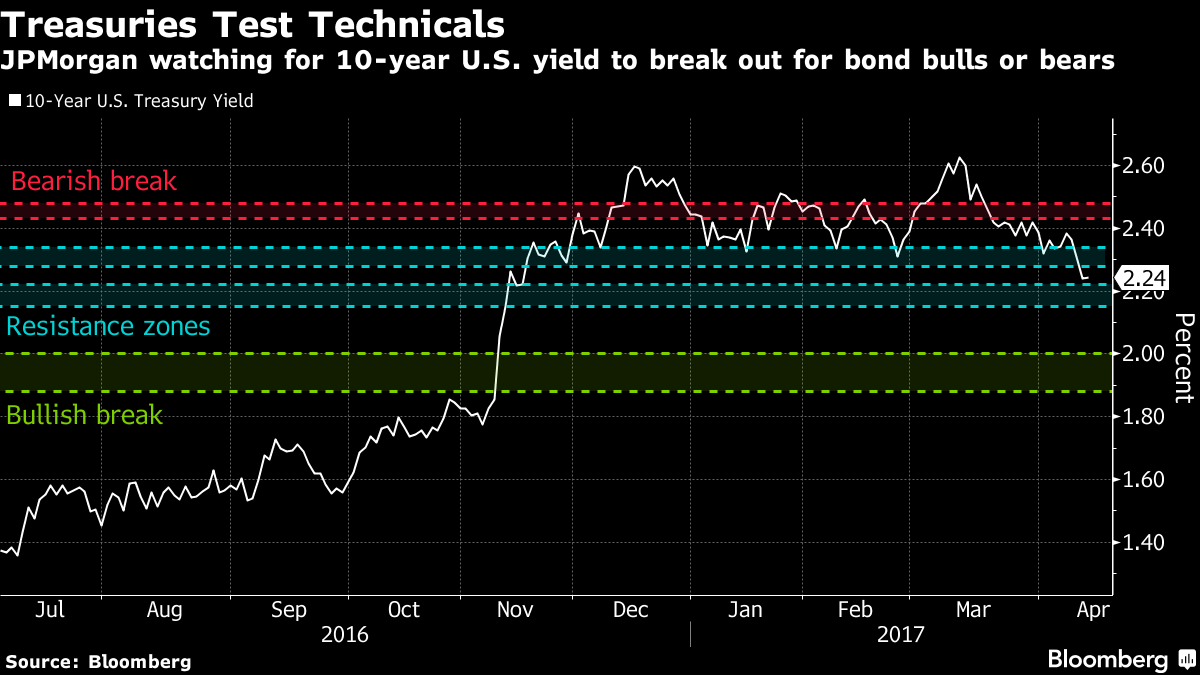

That leaves the benchmark 10-year U.S. yield at 2.24%, near the lowest this year, and the dollar about the weakest versus the yen since November, heading into a relatively quiet week for economic data. Rather than overreact to something like housing starts, traders and strategists are keying in on technical market levels to gauge the sustainability of the latest move.

“North Korea and Syria were the straw that broke the camel's back, but now we have a new range,” said Glen Capelo, a trader at Mischler Financial. He pegs it at about 2.05% to 2.4% for the 10-year yield, after it'd been stuck between 2.3% and 2.65%.

For bond bears, “we're not going to know anything for a while,” on the timing of Trump's fiscal-policy agenda, Capelo said. “The onus now is that the hard data has to turn higher.”

In the meantime, Wall Street strategists are chiming in with their own levels to watch in the trading days ahead.

For the rally to continue, the 10-year yield has to fall below 2.15%, according to JPMorgan Chase & Co. technical analysts Jason Hunter and Alix Tepper. If it does, the yield could plunge all the way back to 1.88%. It'll meet resistance at the 2.34% level on the way up, they said in a note.

Even though technicals back a further rally, targeting the 50% retracement of the Trumponomics sell-off at 2.177%, Ian Lyngen and Aaron Kohli at BMO Capital Markets say they aren't buying it.

“While we'd like to lean more bullishly on the market, the severity of the move coupled with the spike in short-dated implied volatility has us viewing a sideways grinding consolidation as the path of least resistance,” they wrote in a note Friday.

The dollar, for its part, is hovering around its 200-day moving average and its 12-month average closing price, 108.79 and 108.40 yen respectively. A drop in yields could compromise both levels and drag the dollar to as low as 103.33, the first standard deviation from the mean 12-month closing price. Such a fall would align with a roughly 2% 10-year yield.

A decline of that magnitude in the 10-year yield before the end of June would surprise even the most bullish of the 58 analysts surveyed by Bloomberg as of April 13.

As usual, Steven Major at HSBC Holdings is tied for the lowest estimate — 2.2% — when the current quarter comes to an end. He's maintaining a decline to 1.6% by year-end.

Sounds outlandish? Sounds plausible? Well, traders, yields have broken free. Place your bets.

Bloomberg News

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.