It's unsettling that a growing number of Americans are falling behind on their auto-loan and credit-card bills. But it's even more unnerving that analysts seem somewhat surprised by the pace and scope of late payments and losses. Consider private-label credit card company Alliance Data Systems, for example. This week it reported a “dramatic drop” in recovery rates in April, which led research firm Compass Point to question what the lender “may be doing operationally to create so much more volatility in recoveries than its peers,” Bloomberg News reported Tuesday.

Meanwhile, lenders including Santander Consumer USA and Ally Financial have been hit by a surprisingly steep deterioration in consumer creditworthiness. Their share prices have slumped this year as they set aside more money than expected to cover loan losses and update forecasts to include deeper declines in used car resale values.

Capital One and Synchrony recently raised their forecasts for net credit-card charge-offs in 2017, citing weakness among subprime customers rather than their previous rationale of portfolio growth and aging, according to Bloomberg Intelligence.

All this raises the question: Why didn't these financial firms and Wall Street analysts better predict that more consumers would struggle with their bills as they packed on debt and gorged on new cars and trucks? As UBS analysts Matthew Mish and Stephen Caprio wrote in a report on Wednesday, “The worse-than-anticipated performance in auto lending should raise questions around model efficacy.”

It's worrisome to think that big lenders may have failed to sufficiently account for certain borrower behaviors, such as consumers prioritizing their medical bills before auto loans or maxing out their credit-card debt limits while trying to meet all their obligations. But there's also the presence of the type of fraud seen in the last crisis, which is making a bit of a comeback. The UBS analysts said that as many as one in five auto-loan borrowers admitted in a recent survey that their debt applications contained inaccuracies.

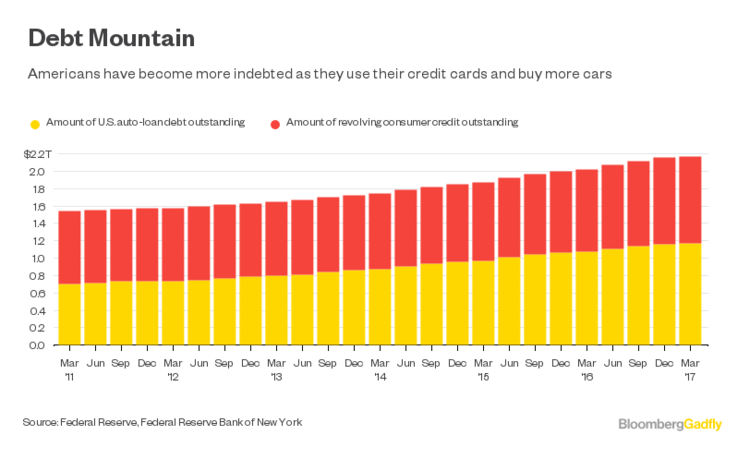

If the models used by the lenders themselves are flawed and based on unreliable data, they will fail to adequately warn of even steeper delinquencies and losses ahead. And this potential blind spot to future losses comes when auto sales are slumping, the economy isn't accelerating rapidly and household debt is reaching a fresh peak.

The UBS report highlights that there's quite a bit of overlap between consumers who have auto loans and credit-card debt, not to mention mortgage, student and medical obligations. Lenders are recognizing this, with Santander Consumer USA recently deciding to stop taking payments by credit cards. Financial firms are also tightening their lending standards, with new car loans for subprime borrowers falling in the first quarter to the lowest in two years, according to data from the Federal Reserve Bank of New York.

It's hard to see how auto-loan and credit-card defaults will lead to a 2008-style meltdown, but it's fairly easy to see how losses could build up, especially as banks cut off credit to the most-indebted borrowers. The big automakers are already reporting declining sales and layoffs. Meanwhile, American consumers won't be able to spring for new purchases if their credit lines are maxed out. This growing spot of distress will bleed into the economy in many ways and will eventually slow growth even further.

Bloomberg News

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.